First published by Tax Planning International: Indirect Taxes, Bloomberg BNA, Volume 13, Number 11, November 2015.

A recent Decree by the Turkish Council of Ministers has introduced additional customs duties for certain goods. However, the legal basis for these duties may be open to challenge. The Council of Ministers in Turkey has issued a Decree (2015/7713; ‘‘Decree’’) which introduces additional customs duties for certain goods in Turkey. However, the additional customs duties arguably run contrary to provisions of the Turkish Constitution, European Union Customs Zone requirements, and a World Trade Organization agreement on information technology.

Since the constitutionality of the Decree may be questionable, parties which must pay additional custom duties based on the requirements of the Decree may consider challenging these taxes with the relevant administration and possibly before the tax courts.

The Decree was published in the Official Gazette number 29379 and entered into force on June 7, 2015.

1. Scope of the additional customs duties

The Decree introduces an additional 30% customs duty on the following goods which hold an ATR Movement Certificate1 and which originate outside Turkey or the European Union:

- “Vacuum cleaners (excluding 8508.70)”, classified under tariff code 85.08.

- “Electro mechanic domestic appliances with self-contained electromotor (excluding vacuum cleaners classified under tariff code 85.08 and 8509.90)”, classified under tariff code 85.09.

- “Electric instantaneous or storage water heaters and immersion heaters; electric space heating apparatus and soil heating apparatus; electro-thermic hair-dressing apparatus (for example, hair dryers, hair curlers, curling tong heaters) and hand dryers; electric smoothing irons; other electro- thermic appliances of a kind used for domestic purposes; electric heating resistors, (excluding 85.54 and 8516.90)”, classified under tariff code 85.16.

The Decree also introduces an additional 10% customs duty on ‘‘parts and pieces’’ for the goods listed above, which are classified under tariff codes 8508.70, 8509.90 and 8516.90.

2. Background to the Additional Customs Duties

It could be said that regulations and impositions related to foreign trade and taxation of electronic devices have significantly increased since a major Turkish consumer electronics company applied in December 2014 to initiate a safeguard investigation regarding mobile phone imports. The Turkish manufacturer intended to enter the smartphone market, planning to release a new smartphone model in 2014. The manufacturer alleged that smartphone imports had increased excessively, causing serious injury (or threat of injury) to the domestic industry.

As a result, Turkey’s Minister of Economy (Mr. Nihat Zeybekçi) publicly announced in December 2014 that the ministry had received many complaints about mobile phone imports from domestic manufacturers. The Minister stated that the ministry was aware of foreign subsidies and incentives which caused unfair competition and that Turkey would take the necessary steps to counter this. The Minister noted that if foreign manufacturers of these goods wished to avoid additional customs duties, they should directly invest into Turkey and manufacture the products locally.

The Minister’s comments appeared to reveal the government’s intention to decrease unemployment rates and increase tax revenues through establishing and encouraging local industry. However, questions were raised about the real economic reason behind the safeguard measure investigation, with suggestions that Turkey aimed to reduce its import volumes, to keep pace with decreasing export volumes. Some commentators argued that the Turkish government intended to reduce its current account deficit by imposing new taxes or financial liabilities on imported goods. On balance, this seems to be the most logical conclusion, given that Turkey’s current account deficit has been increasing and has now reached approximately $45 billion.

While the story originated on the basis of mobile phone imports, the focus of attention has changed. The Minister of Economy has on several occasions indicated that imports of consumer electronics and home appliances are also harmful to local manufacturers on the basis that they cause a decrease in sales. In addition, the Minister stated that Turkish manufacturers had requested at least 30% extra customs duty or additional financial liabilities to be imposed on such imported items in order for Turkish manufacturers to survive.

The logic behind the investigation initiated concerning the import of mobile phones, and the ministerial comments over the need for protection in relation to the local consumer electronics and home appliance sector, is puzzling given that Turkish domestic players are quite strong, not only in Turkey, but also in the global consumer electronics and home appliance sector. In fact, several domestic brands such as Vestel and Beko lead the Turkish sector as well as exporting a large amount of products across the world. Vestel is a Turkish home and commercial appliance manufacturing company, specializing in electronics and major appliances. Beko is also a leading Turkish company in the electronics and white goods sector. Both Vestel and Beko hold significant shares of the European consumer electronics and home appliance markets.

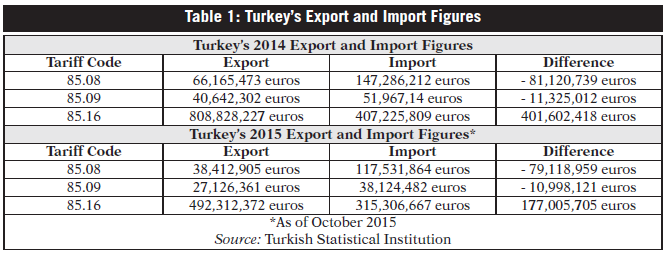

In accordance with the figures in Table 1 (Source: Turkish Statistical Institution), and given that the relevant goods are generally manufactured by the same producers, Turkey’s export figures for 2014 and 2015 reveal a healthy and well-operating domestic industry in Turkey. Moreover, Vestel and Beko also produce other home appliances, such as televisions and refrigerators; in this context, Turkey exported 1,442,881,400 euros-worth of televisions during 2014, as well as 1,516,38,671 euros-worth of refrigerators and deep freezers.

Statistics also show that Turkish manufacturers dominate the consumer electronics and home appliance market within Turkey, with Turkish consumers preferring local brands to foreign imports. For example, a total of 8.3 billion Turkish liras-worth of refrigerators was sold in Turkey in 2014, including 6.7 billion Turkish liras-worth of products (81%) sold by domestic manufacturers.

Accordingly, given the market shares and recent import/export volumes, the additional customs duty imposed on goods classified under tariff codes 85.08, 85.09 and 85.16 does not obviously represent a move to protect the domestic industry. Rather, this can more logically be interpreted as an attempt to reduce the national deficit through revenue gathering.

3. Council of Minister’s Legal Power to Impose Taxes

The Turkish Constitution states that taxes, fees, duties and other such financial obligations must be imposed, amended, or revoked by law (Article 73). Therefore, taxes must be based on a law enacted by the parliament. The Council of Ministers is not empowered to impose new taxes via Decrees.

However, the Constitution allows the Council of Ministers to amend the percentages of exemptions,

exceptions and reductions for taxes, fees, duties and other financial obligations, within certain legislative limits. Therefore, the Council of Ministers can legitimately change the percentage of an existing tax, provided the change remains within legislative limits and it has been granted this authority.

The Constitution also empowers the Council of Ministers to impose additional financial liabilities on imports to regulate foreign trade, but it specifically excludes imposing new taxes (Article 167). The concept of ‘‘additional financial liability’’ is relatively narrow and well-defined under Turkish legislation. It does not include taxes and additional customs duties, which can only be imposed by law.

The Decree identifies Article 2 of the Law on Customs Entry Tariff Schedule numbered 474 as its empowering legislation. The empowering article enables the Council of Ministers to amend the customs duty percentage by up to 50% for goods listed under the Customs Entry Tariff Schedule. The article’s wording clearly empowers the Council of Ministers to amend an existing percentage, but not to impose a new financial obligation. Despite this, the Council of Ministers has introduced a new obligation alongside existing customs duties, rather than increasing the percentage of existing customs duties.

Accordingly, a strong argument exists that the financial obligation introduced by the Decree is a new tax, as opposed to a percentage increase for an existing tax or an additional financial liability. This interpretation is supported by the Decree identifying the new obligation an ‘‘Additional Customs Duty’’. Further, the Decree does not mention any changes to existing percentages, but rather introduces a separate and additional customs duty.

4. European Union Customs Zone

Turkey has been included in the European Union Customs Zone (‘‘Customs Zone’’) since December 1995 (Association Council Decision numbered 1/95, within the scope of the Ankara Agreement between Turkey and the European Economic Community). Membership allows free trade between Customs Zone countries without being subject to any customs duties or tariffs. Members can also determine mutual trade policy and tariff applications for imports from third countries.

Customs Zone countries (including Turkey) cannot impose duties or similar financial liabilities on goods which have entered free circulation within the Customs Zone.

Under Turkey’s arrangement with the European Union, products from third countries will be considered to be in ‘‘free circulation’’ if the following criteria are all met:

- import formalities have been complied with;

- customs duties or charges of equivalent effect have been levied, either in the Customs Zone or in Turkey; and

- the exporter has not benefited from a total or partial reimbursement of duties or charges.

Exporters issue an ATR Movement Certificate in order to benefit from the exemption. Any goods carrying an ATR Movement Certificate are accordingly deemed to be in free circulation. Therefore, customs duties or similar taxes cannot be requested for goods carrying such certificates.

Accordingly, the additional customs duties introduced in the Decree arguably run contrary to the exemption from custom duties which applies to goods in free circulation within the Customs Zone, which did not originate from the European Union or Turkey.

5. The World Trade Organization’s Information Technology Agreement

On July 24, 2015, members of the World Trade Organization agreed in Geneva to expand the scope of the Information Technology Agreement and to remove customs duties applied to high-tech products. The parties undertook to eliminate the customs duty within three years. The intention is that consumers’ costs will decrease and consumers will benefit from innovative products.

The introduction by the Decree of an additional customs duty in Turkey therefore ostensibly contradicts Turkey’s international undertakings to eliminate customs duties on high-tech products. Finally, it remains to be seen whether the Decree’s requirements will stand up to legal scrutiny and challenges from parties which may now receive significantly reduced economic incentives to trade these goods in the Turkish market.

1. The ATR Movement Certificate entitles goods, which are in ‘‘free circulation’’ in the EU (i.e. the goods are EU originating, or on importation into the EU all the relevant duties and taxes have been paid) to receive preferential import duty treatment when shipped to Turkey.